As ace investor Warren Buffet likes to put it, “If you don’t find a way to make money while you sleep, you will work until you die.”

The “make money work for you” phrase is an inch away from becoming a cliché. Everybody wants to amass wealth while getting their Zs and waking up with more cash in the bank than they had before going to bed.

There is no silver bullet to achieve this freedom or a magic formula that gives investors a single answer. Instead, there are a couple of methods that you can use in combination to deploy funds and earn returns without putting in any work.

Investors must, however, always remember to assess their risk appetite before putting money into any of these asset classes.

It’s assumed here that investors have the required insurance policy set up prior to investing.

Our recommendations are in order of risk—high risk, high return asset classes listed first.

5 Ways to put your money to work

- Invest in (Not Trade) Cryptocurrencies

The buzz around cryptocurrency has recently spiked. It had been building momentum since the beginning of last decade, but it now has enough investor confidence to actually produce massive returns.

It’s recommended to NOT trade cryptocurrencies because their volatility can quite easily leave investors with less money than they put in. Instead, investors should use a fundamental approach. Investors must base their decisions on fundamental factors that drive the price of any cryptocurrency—the biggest price-driver for cryptos is demand.

So, what’s hot right now?

Everybody knows about Bitcoin and Ethereum, but few know about their not-so-popular (at least yet) cousin, Chainlink. Before talking about how to buy Chainlink, let’s talk about why it could be a good way to deploy money.

Why is Chainlink good?

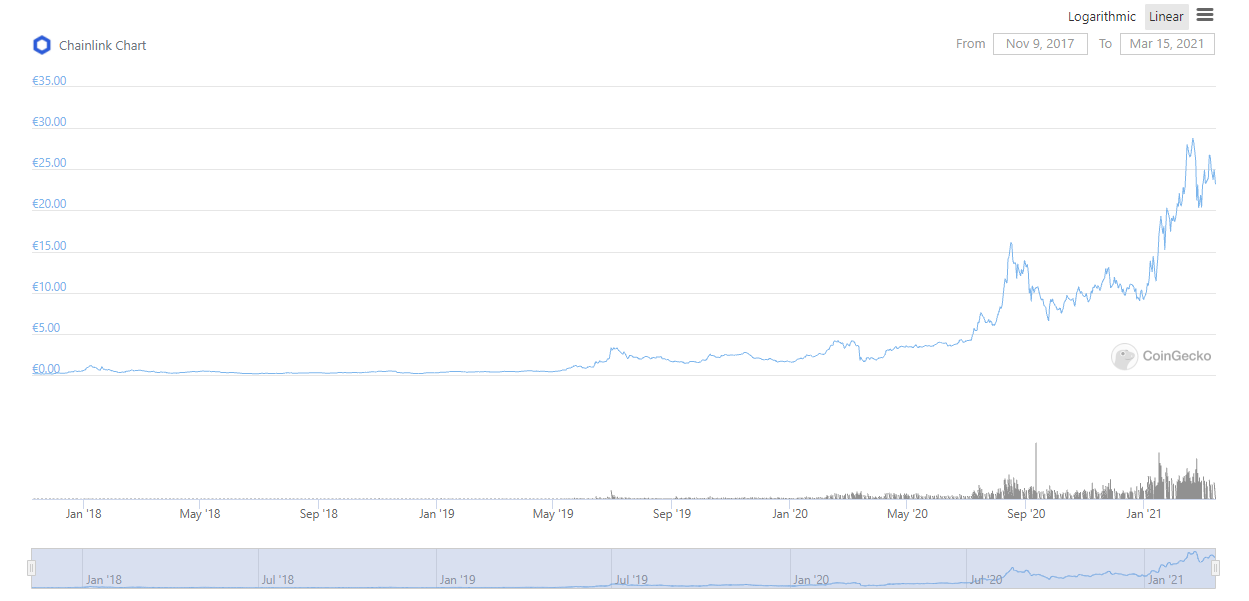

Let me give you some data points and a visual. Here’s how much the Chainlink earned for investors over the mentioned time frames:

| 7 days | 14 days | 30 days | 1 year |

| -3.2% | 13.9% | -8.1% | 1113.4% |

Here’s what can be construed from this data:

- The prices can be extremely volatile. If you had invested €100 a month ago, you would now be left with €91.9. If you had invested €100 last year, you would now have €1,113.4. This highlights why investment can be more fruitful than trading.

- Chainlink prices only started to gain traction around August 2020. The prices have come down from their all-time-high, which means this could be a good time to open a position in Chainlink.

The how to buy Chainlink tutorial is a one-liner: you can buy Chainlink from a cryptocurrency exchange, just like Bitcoin or Ethereum.

I reiterate the importance of realizing your risk appetite beforehand. Cryptocurrency is currently the riskiest asset class. If done right, though, it can make you colossal wealth.

- Become a Sleeping Partner in a Business

Next on our risk spectrum are the economy’s money-making machines—businesses. Investing in a business can offer extremely high returns because you assume a lot more risk than investing in a mutual fund or fixed deposit. The smaller the business, the higher the risk.

Another thing to note here is that as a sleeping partner, the investor may not be an active participant in the firm’s day-to-day activities. So, it’s important to come to terms with the fact that you will have little control over the business’ operations.

Let’s nail some basics:

- Limit the liability: Partners of a partnership firm are personally liable in case of bankruptcy. It is always prudent to limit the liability while drawing a partnership deed. It’s best to have a professional take care of this.

- Due diligence: Businesses can be vulnerable to several kinds of risk including operational and financial risk. Before investors put their hard-earned money into a business, they must analyze the financial statements to gauge the potential return on investment. During the analysis, investors should pay due attention to not just general, but industry-specific risks as well.

- Are the partners trustworthy?: As a sleeping partner, an investor will have a minimal role to play in the business. Investors will leave their money in the hands of other active partners. Unless there is trust among the partners, it is unlikely that the partnership will last long.

Owning a business can generate one of the greatest ROI digits for investors in the long run. Take the leap of faith only when you’re completely confident, though. Investment in a business is illiquid, so investors looking for a short-term or liquid investment may want to look at other options in the list.

- Alternative Investments

Alternative investments include real estate, art, private equity, and the like. These investments are risky and illiquid. Selling a house takes months, if not years. Given their high risk, they also have the potential to generate mammoth returns.

There is also a barrier to entry with alternative investments because they often require a large amount. This issue has been partly done away with for real estate investments with the growing popularity of REITs, though. Think of REITs as a mutual fund for real estate. They offer liquidity and make real estate investment accessible for small investors.

The latest wave in alternative investments is non-fungible tokens (NFTs). An NFT is a blockchain-linked digital asset that is generated cryptographically. In fact, just 6 hours prior to this writing, Elon Musk (who else!) tweeted out that he is selling an NFT-themed song about NFTs via NFT.

Note that this is not the most ideal category for beginners. Beginners are better off with mutual funds and fixed-income investments. Speaking of which…

- Invest in Equities and Mutual Funds

For investors keen on investing in a business while still retaining the ability to liquidate in minutes—equities are a perfect fit.

When you invest in the equity of a corporation, you derive the benefits of the business, and you reserve an option to exit the minute you feel you want out.

Why are equities listed after business in terms of risk?

Equities are high-risk assets too. However, investors can diversify their equity investment portfolio far more easily than they can diversify their business’ product or service portfolio.

Many investment platforms will give investors their portfolio’s standard deviation as a measure of risk. That being said, this is a dynamic number that changes with changes in factors like the country’s economic landscape, industry regulations, or just the market’s “sentiment.”

A shortcut to managing risk

Adriaan Van Ketwich, a Dutch businessman, introduced the world to its first mutual fund in 1774 precisely for this reason. Most investors can’t actively manage their portfolio–some lack knowledge, and some, time.

Mutual funds are managed by qualified investment professionals appointed by the fund house (or AMCs, i.e. Asset Management Companies). They operate under a regulatory framework established by the country’s governing body (FCA in the UK). Put simply, mutual funds pool money from investors and invest it in equities (or bonds). They charge a small fee for this, but it is rarely a significant amount unless your investment is in millions.

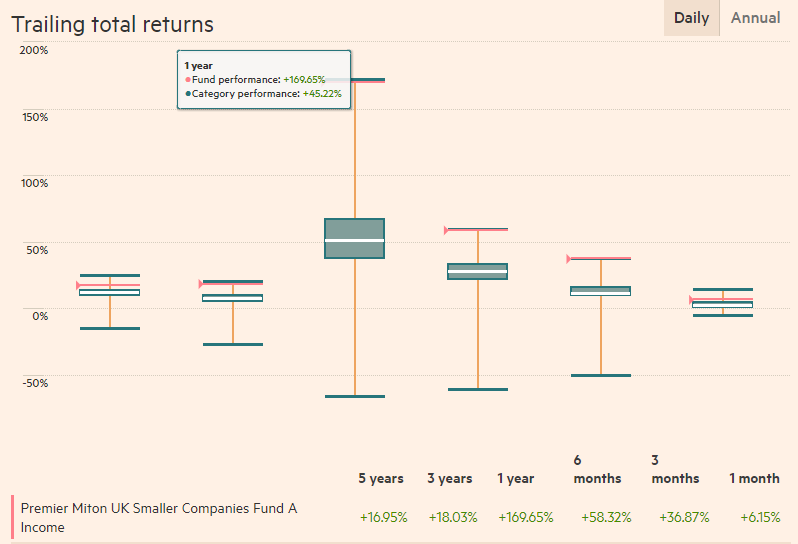

Evidently, mutual funds can make smart investors a lot of money:

An investment worth £100 in Quarter 1, 2020 in the Premier Miton UK Smaller Companies Fund would have grown to £240+ in a year. That’s more than a 100% return on investment! To be precise:

That being said, the Premier Miton UK Smaller Companies Fund is a high-risk fund given it invests in small companies, and therefore, the returns generated over various timeframes may fluctuate significantly.

Investors who are wary of the fees charged by AMCs may want to consider investing in Index funds. These funds are passively managed and track a benchmark index, like the FTSE SmallCap.

- Invest in Fixed-Income Securities

This is where investors would want their money to be if they’re closer to retirement. Even young investors should have some fixed-income investments in their portfolio to keep the portfolio’s standard deviation in check.

Investors may choose to invest in these fixed income securities, as listed in order of risk and return potential, with high-risk securities listed first:

- Corporate Bonds (maybe further classified in terms of risk with ratings like AA, AAA, etc.)

- Long-term debt mutual funds

- Short-term debt mutual funds

- Government Securities

- Fixed Deposits, Recurring Deposits, Savings Deposits

The driver of risk and return for fixed income securities is its duration and rating. Duration is a metric used to measure the risk of fixed income securities, while a rating is assigned to fixed income securities by credit rating agencies like S&P and Fitch Ratings.

- Double Down on Debt

A penny saved is a penny earned. Always consider the opportunity cost of investing in any securities discussed above. If an individual has savings worth €1,000 that he wants to invest in equities with a target return of 12% p.a., while he’s paying interest at the rate of 20% p.a. on his credit card debt, his opportunity cost of investing in equities is 8%.

In simpler words, using those €1,000 to pay off the debt will leave him with more money in hand than investing that money in equities.

The only place you should put your money in when you have outstanding debt is insurance.

Conclusion

Making your money work has become astonishingly simple over the past few decades. You can invest or redeem your investments at the press of a button, and access information whenever you need it.

Before you hop onboard the investment train, make sure you have the 2 essential elements of the equation figured out: insurance and debt. The first step is to make sure that you have a life and health insurance policy to take care of your family even in your absence. Next, fight out any debt that is eating away your income.

When you have insurance coverage and are debt-free, you can make your money multiply without even moving.

Bitcoin

Bitcoin  Ethereum

Ethereum  Tether

Tether  XRP

XRP  BNB

BNB  Solana

Solana  USDC

USDC  Cardano

Cardano  Avalanche

Avalanche  Toncoin

Toncoin