Asset Allocation preferences follow the life-cycle theory of human beings.

The Life cycle theory says that your propensity to assume risk is higher in your younger years and reduces as you grow older. You become more conservative in your outlook with age.

Age group between 20 and 40 years

As you are younger, you are looking at longer working life at the beginning of your career. Any investments you make have a more extended period to recover from market fluctuations and pass through various business cycles. You also have a greater propensity to assume risk.

Accordingly, your portfolio allocation is more towards risky assets and less focused on conservative assets. Your asset allocation is more geared towards equities and less towards bonds, savings deposits and other such assets.

Age group 40 years and above

As you grow older and approach your 40s, you grow in your professional career, reaching higher levels of salaries and perquisites. Your family also grows and your children begin pursuing higher education. Your emoluments grow along with your personal expenditure demands. You have been steadily savings for the past 20 years in high growth assets and have accumulated a sufficient corpus. But your personal expenditures are also keeping pace. At this stage, when you are in your 40s, you are still facing another 20 years of a professional career with steady and growing cash inflows.

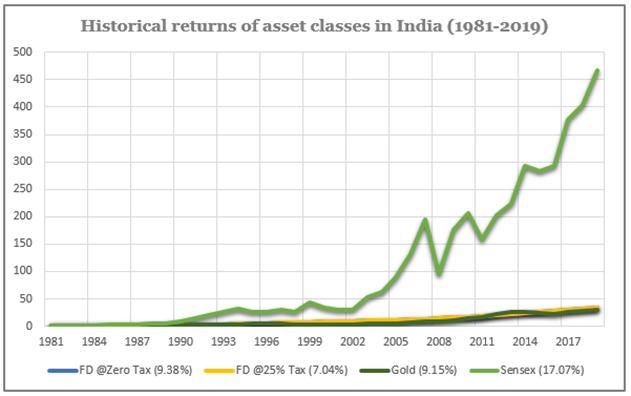

The historical returns on the various asset classes are given below:-

The compound annual growth rate of the various asset classes have been as follows:-

| Asset-Class | Rate of return p.a.(%) |

| FD pre-tax | 9.38% |

| FD Post-tax | 7.04% |

| Gold | 9.15% |

| Sensex 30 | 17.07% |

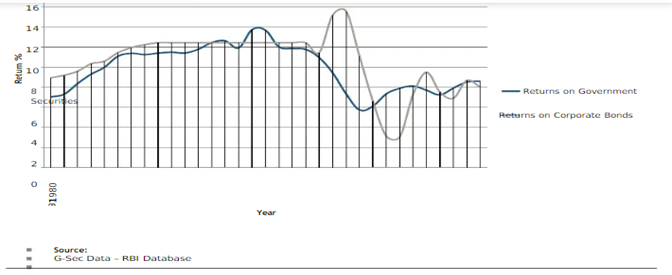

| Government Bonds | 7%- 13.5% |

| Corporate bonds | 7%- 15% |

| Indian Real estate | 15% |

As can be seen from the above graph, stock market investment i.e equity market have the highest compound annual growth rate during the period under consideration, while fixed deposits have the lowest rates.

Asset Allocation for a 40-year-old professional could look like this:

| Asset Class | Conservative Allocation | Aggressive Allocation |

| Equities and equity linked products | 55% | 72% |

| Government bonds and Corporate Bonds | 20% | 10% |

| FD post-tax | 8% | 5% |

| Gold, commodities | 4% | 5% |

| Indian Real estate | 13% | 8% |

| Total | 100% | 100% |

You can position yourself anywhere in this asset-allocation continuum. The higher your relative allocation to equities, the higher the risk-adjusted return and wealth maximisation will be. Self-owned real estate forms a part of the asset allocation as it forms a part of your net worth. No asset class is devoid of risk; even bonds and fixed deposits are subject to interest-rate risk.

You can calculate your risk-adjusted return from the above tables and see which scenario results in the highest risk-adjusted portfolio return. Also, your portfolio returns have to be adjusted for inflation. When inflation is high in the economy, the return on bank FDs drops considerably. Also, proper research and due diligence must be conducted when investing in equity-linked products and ensuring appropriate diversification of portfolio assets.

Long-term wealth maximisation is aimed to help you maintain your preferred standard of living and remain independent during the post-retirement years.

Bitcoin

Bitcoin  Ethereum

Ethereum  Tether

Tether  XRP

XRP  BNB

BNB  Solana

Solana  USDC

USDC  Cardano

Cardano  Avalanche

Avalanche  Toncoin

Toncoin